Spending Update 2018

I last posted a spending update almost two years ago, so it seems like time to do another one. We're still living in Somerville, with housemates and tenants. At the beginning of this period we were out of our house for several months because we were adding dormers, which we finished a bit over a year ago. With the extra space, we're now able to have an au pair, plus Anna isn't sleeping in our bedroom anymore.

In terms of accounting, we've switched from tracking everything via spreadsheets to using a mix of spreadsheets and Mint. Mint can pull transactions directly from our bank account and credit cards, which means we're much less likely to accidentally skip something. On the other hand, it's easier for things to be incorrectly categorized and harder to annotate transactions carefully or write custom logic. Now we're categorizing every transaction in Mint, and then additionally using spreadsheets as needed. Currently that's keeping track of allowance spending, where we want to keep to a specific budget that accumulates if unspent, and keeping track of things for taxes (house spending, contra dance musicianing).

We started using Mint on 2017-05-01, so I'll look at things on a one year basis from there, and then correct in places where this isn't accurate. For housing I'll use a completely different approach, where I amoritize all large expenses over 30 years and treat them as if we'd financed them along side our mortgage. [1]

Housing: $2,750/month

One time expenses (all time)

Purchase and all one-time expenses included last time: $915k

Adding dormers: $110k

Replacing front porch: $18k

Ceiling soundproofing: $1.8k

Partitioning home office: $900

Replacing garden wall: $700

Installing sump: $300

Other: $10k

Ongoing expenses, all whole-house (including tenants' unit):

Other: $550/month

Electricity: $300/month

Water/Sewer: $150/month

Gas (Heat): $150/month

Rent income: $4.2k/month

Kids:

Childcare: $20.4k ($81/day; $41/kid-day)

Most of this is an au pair, with occasional payments to other people for babysitting.

Gear/nursery: $0.5k ($20/kid-month)

Other: $210 ($9/kid-month)

Clothes: $103 ($4/kid-month, but some kid clothes were hand-me-downs and some came out of Julia's allowance)

Taxes

Income tax: $1.4k/month

State tax: $1.1k/month

Social Security tax: $1.3k/month

Medicare tax: $350/month

Retirement: $1.5k/month (401k)

Personal: $480/month ($55/week each, for entertainment, clothes, etc)

Medical: $950/month (excludes portion work paid)

Donations: $11.8k/month (50% of 2017 income)

Loan Interest: $160/month (pulling some donations ahead a year)

Food: $750/month ($250/adult, $150/person)

Transportation: $77/month

Some MBTA, some Uber, some car rental, some gas for borrowed cars. I have a T-pass covered by my work, which would cost $89/month if we paid for it.

Vacation: $3k (we went to Puerto Rico in March with Julia's family)

Other: $83/month

In simple form, monthly numbers:

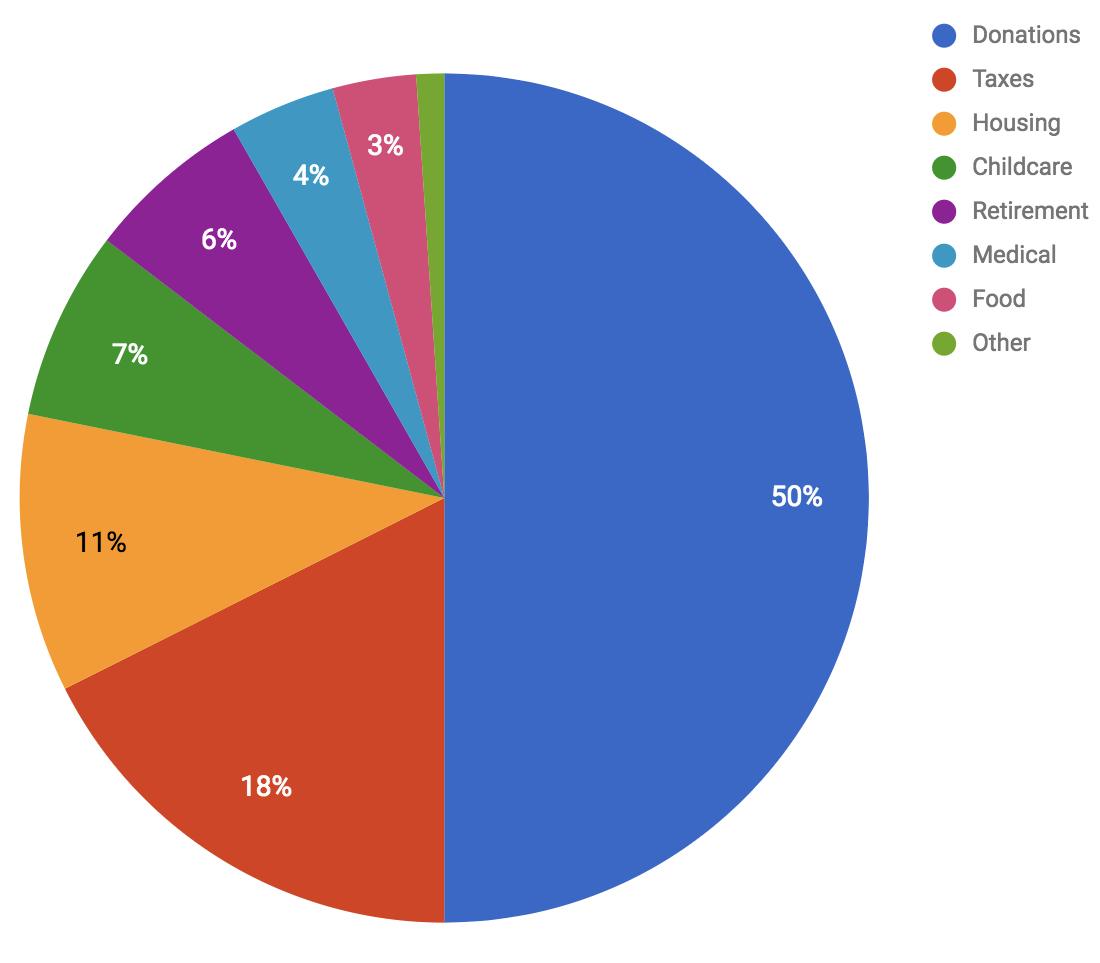

Donations $11,800 Taxes $4,150 Housing $2,750 Childcare $1,700 Retirement $1,500 Medical $950 Food $750 Personal $480 Vacation $250 Interest $160 Other $230

And as a chart:

Comparing with last time, still all monthly numbers:

Donations $12,200 → $11,800

Still 50% of income, but I earned less because I spent part of the year at a startup and part of the year unemployed

Taxes $4,140 → $4,150

Taxes went up slightly because more of our rental income is taxable, because with the dormers more of our house is occupied by us instead of people who pay us rent.

Housing $2,230 → $2,750

Most of this increase is the cost of adding dormers, porch, etc, which I'm amortizing over 30 years. [2] Some of it is also that in the previous period I didn't yet have good estimates for utilities and lowballed all of them significantly. Our utilities are slightly lower than they were in 2016. We also take in more in rent than we did then, which makes this increase smaller than it would be.

Childcare $3,470 → $1,700

The big decrease here comes from switching to an au pair. But some of that is offset by higher housing and food costs. Say they're 25% of our spending here (one of four bedrooms, one of four people eating if you count the kids as halves) then $1,700 becomes $2,500, which is still very good for two kids in this area.

Retirement $1,500 → $1,500

Still taking the full pre-tax allowed amount.

Medical $370 → $950

My employer's costs have gone up, and we're paying a perecentage of that. Plus we had some months where we paid full price for private insurance when I was unemployed.

Food $230 → $750

Some of this is an extra adult (au pair), some is that the kids are eating more, and some is that Mint is probably doing a better job keeping us from excluding things accidentally, but I also think we've shifted to somewhat more expensive food.

Personal $390 → $480

We raised our allowance budgets from $45/week to $55/week.

Vacation $0 → $250

Previously we'd generally paid for vacations out of our personal spending budgets, and done pretty cheap things. We decided that this was something we wanted to spend a bit more on as a family, and not trade it off explicitly against day to day self-spending.

[1] This is the same thing I did (last time): treat one-time expenses as if we had financed them as part of the same 30-year fixed rate mortgage we used to buy the house, add in ongoing expenses, and subtract rent payments from tenants and housemates. The idea is, the house cost $800k with a $600k mortgage, and our mortgage payment is $3,600/month. The mortgage payment includes $700/month of property taxes and insurance, so set that aside and we have $2,900/month. Comparing the mortgage amount to the monthly payment, for every $1000 of one-time expense you can think of there as being a $4.83 monthly payment. The down payment ($200k) and other one-time expenses ($255k) bring this imaginary mortgage from $600k to $1M and would give a mortgage payment of $5,100 for the whole house. Add back in the insurance and property taxes ($700), and $1,150 in other monthly expenses: heat, water, electricity, repairs, etc, and you have $7000 as the monthly cost of the house. Then subtract $4,200 in rent income, leaving $2,750/month.

When I did this last time I didn't subtract off the escrow portion of our mortgage payment and put it back. Doing that instead brings last time's numbers up by $360/month, from $1,870 to $2,230.

[2] As before, not all of this is "real" spending: some of it is effectively investment, since the house will still have value at the end. If you "mark to market" and consider that the area has become much more valuable while we're living here there's a sense in which our housing has actually been nearly free.

Comment via: google plus, facebook